Strategic Financial Planning Beyond Traditional Advisory Services

We’ve all seen the classic image of financial planning: a serious office, stacks of papers, and a chart predicting a hazy future. For years, that model, centered mostly on picking investments and yearly check-ins, was the norm. But when money touches every part of our lives, an annual review starts to feel pretty outdated.

Real financial security isn't just about choosing the right investments. It’s about building a flexible plan that connects all the pieces of your life. It’s moving from getting advice on one puzzle piece to having a partner who helps you see and shape the whole picture.

The Limits of the Traditional Model

Let's give credit where it's due. Traditional financial advice has done a lot right; it’s brought structure to saving, expertise to investing, and a vision for retirement. But today, it’s showing its limits:

The Silo Problem: Your investments, taxes, and estate plan are often handled by separate people who don't talk to each other. So, a smart investment move might backfire at tax time.

It's Reactive: Advice tends to come after the market shifts, or once a year, rather than before life happens to you.

It Focuses on Products: Conversations often center on what to buy, a specific fund or policy, rather than how everything works together for you.

The New Blueprint: Integration Under One Roof

The antidote to fragmentation is seamless integration. The most forward-thinking firms are breaking down the walls between different financial disciplines, acting as the central hub for your entire financial life. Take, for example, the philosophy of a firm like Confidence Wealth Management, whose high-value boutique firm intelligently constructs your wealth plan, coordinates the completion of your tax return, and helps prepare your estate planning documents, all under one roof, seamlessly integrated so people can focus on enjoying life. This model creates powerful synergies:

Tax-Aware Investing: Your investment manager and tax preparer are, in effect, the same team. They can strategically harvest investment losses to offset gains, optimize account types (Roth vs. Traditional), and structure income in retirement to minimize tax brackets.

Estate-Plan-Aligned Assets: Titling of accounts and beneficiary designations are coordinated with your actual trust or will documents, preventing a costly and emotionally draining probate process that can invalidate careful planning.

Real-Time Strategy Adjustments: A major life event triggers a coordinated review across all disciplines immediately, not six months later when tax season rolls around.

The Core Pillars of Strategic Financial Planning

So, what does this integrated approach actually look like in practice? It’s built on several key pillars that go far beyond portfolio management.

Holistic Life and Goal Mapping

This is the foundational step. It’s not about how much you have, but what you want it to do for you.

Deep-Dive Discovery: Conversations explore values, family dynamics, career aspirations, and legacy wishes, not just numbers.

Goals with Nuance: Instead of just "retire at 65," planning for a phased retirement, a sabbatical, funding a grandchild's education, or launching a passion project.

Liquidity Planning: Strategically mapping out when you will need cash flow from your investments, so money isn’t trapped in the wrong places.

Proactive Tax Strategy

Tax planning is no longer an annual compliance task; it's a year-round wealth preservation strategy.

Charitable Giving Strategies: Using tools like Donor-Advised Funds (DAFs) or gifting appreciated stock to maximize impact and tax benefits.

Retirement Distribution Planning: Crafting a precise, multi-year plan for drawing from taxable, tax-deferred, and tax-free accounts to minimize lifetime taxes.

Business Owner Optimization: For entrepreneurs, integrating entity structure, compensation, and exit planning with personal financial goals.

Dynamic Estate and Legacy Coordination

This ensures your wealth translates into your intended legacy, without family conflict or high legal costs.

Document Coordination and Review: Regularly updating wills, trusts, powers of attorney, and healthcare directives as laws and your life change.

Beneficiary Alignment Audits: Ensuring all financial accounts and insurance policies are correctly titled and aligned with your trust documents.

Family Education and Communication: Facilitating structured conversations to prepare heirs, discuss values, and ensure a smooth transition.

Risk Management as a Strategy

Looking beyond basic insurance policies to protect your entire financial ecosystem.

Liability Analysis: Reviewing umbrella insurance needs in the context of your total net worth and lifestyle.

Long-Term Care Integration: Evaluating funding strategies (insurance, hybrid products, self-funding) as a core part of the retirement plan, not an afterthought.

Business Continuity Planning: For owners, ensuring personal and business finances can withstand the loss of a key person or a forced sale.

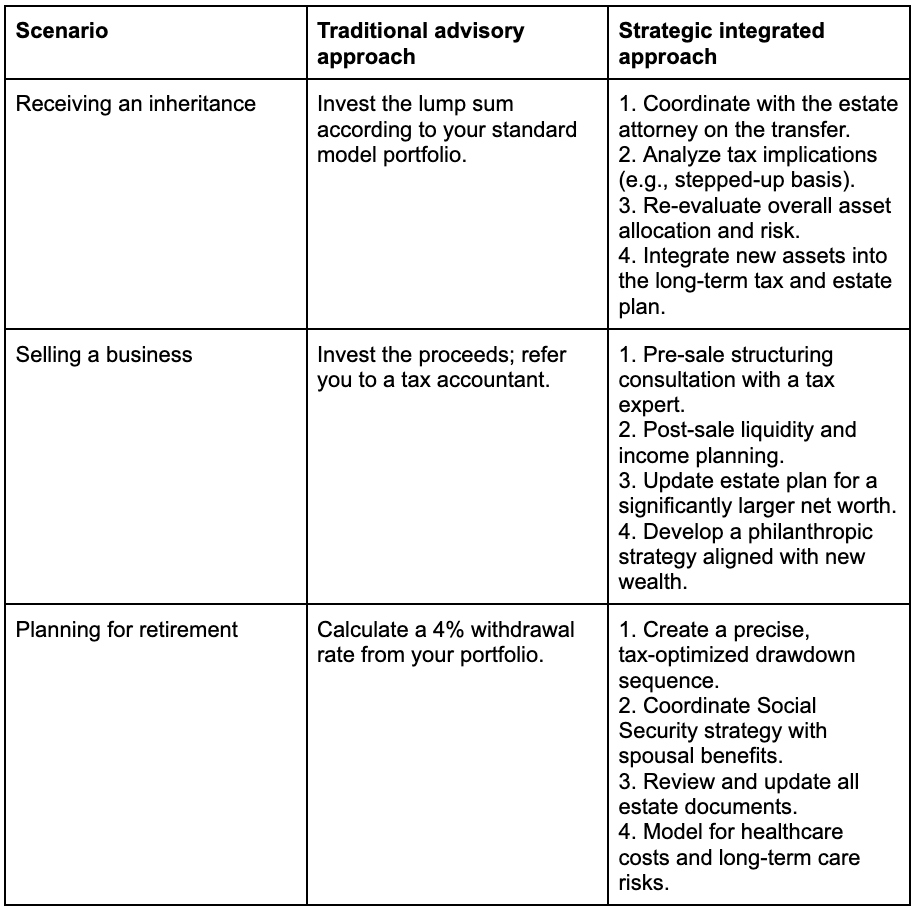

Seeing the Difference

The contrast between traditional and strategic planning becomes clear when you look at how they handle real-life scenarios.

Finding the Right Partnership for You

Moving to this kind of comprehensive planning is a significant step. How do you identify a firm that can deliver it?

Look for a Fiduciary, Always: They are legally obligated to put your interests first.

Ask About Their "Team": Who are their in-house or deeply trusted partners for tax, legal, and insurance? How do they communicate?

Demand a Collaborative Process: The plan should feel like a co-created roadmap, not a delivered product.

Evaluate Their Technology: Do they offer consolidated reporting that shows your entire net worth, not just the assets they manage?

Listen for "Why": Advisors should be more interested in your "why" than your "what."

In the end, strategic financial planning beyond traditional services isn't about more complexity. It's about achieving a simpler, more secure reality. It’s about building a framework that allows you to make life decisions with financial confidence, knowing you have a dedicated team ensuring all the pieces move with you. That’s the true definition of wealth management in the modern age.