How Small Firms Can Design Health Plans for Employees and Their Spouses

Many professionals don’t make career-related decisions purely based on their core job profiles. They also consider the workplace: its environment, culture, and the support the employer provides. Health insurance and related plans comprise a substantial part of these sought-after benefits.

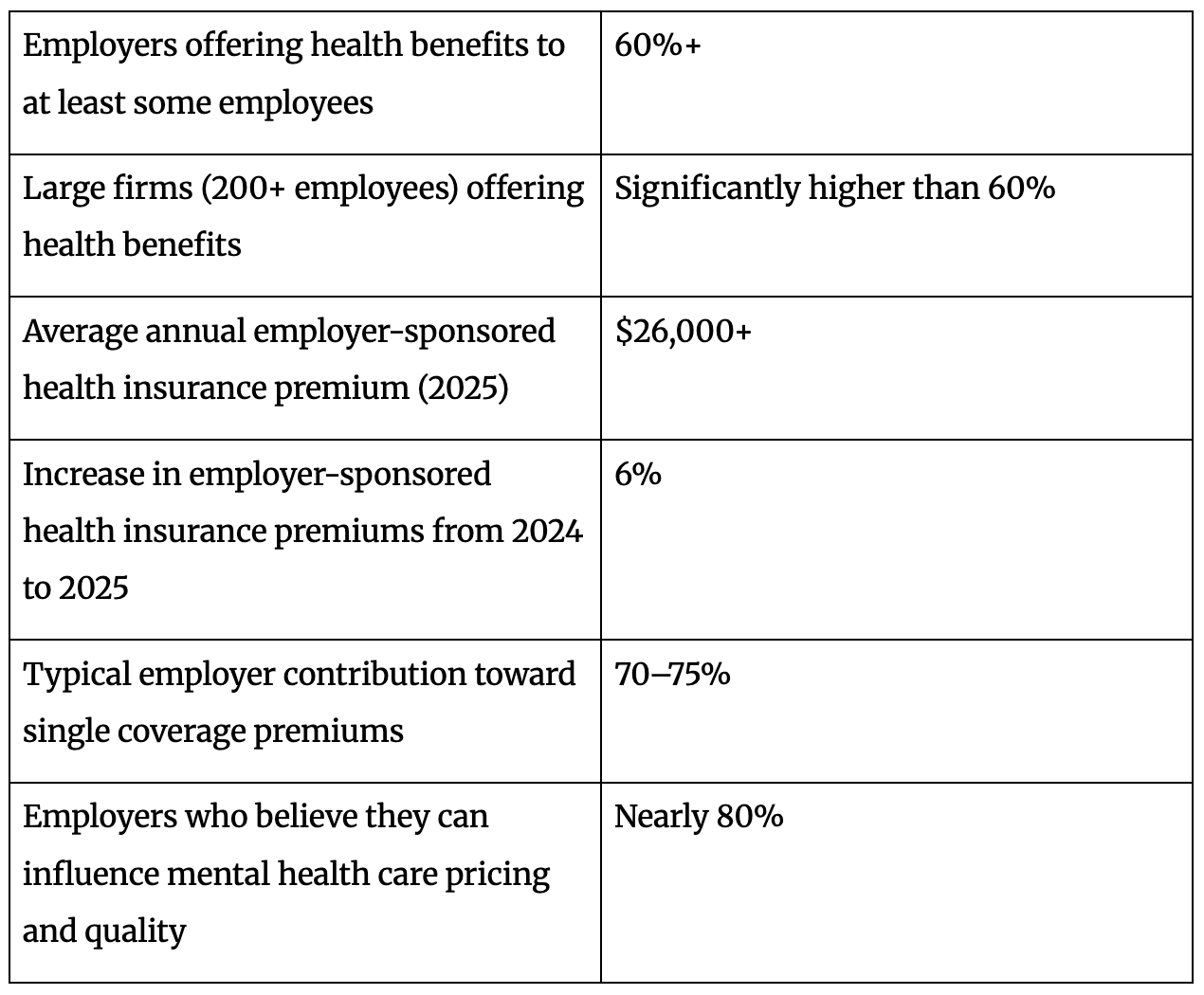

Industry reports indicate that over 60% of firms provide health benefits, at least to some of their employees. Of course, the percentage is much higher for bigger firms that have 200 or more workers. Besides supporting the employee, many of these plans also include the immediate family.

As a small business owner, designing and offering health and wellness support can be challenging but rewarding. A good place to start is with assessing the specific requirements of your team members. For instance, the health demands of workers in a polluted industrial area will be very different from those in a corporate office uptown.

Once you have this understanding, consider the guidelines below to develop powerful, sustainable health plans.

Explore Various Cost-Sharing Arrangements

For small businesses, employee insurance coverage constitutes a significant expense. Their pockets aren’t as deep, and brand equity may not yet be established enough for employee loyalty. This is why arriving at the best-fit cost-sharing arrangement is crucial for a sustainable plan.

KFF’s 2025 survey on employer health benefits found that annual premiums have been increasing for employer-sponsored health coverage. It crossed $26,000 in 2025, which was 6% higher than in the previous year. Typically, employers cover 70 to 75% of single coverage, although this depends heavily on the firm size.

You cannot rush through this process of identifying the split of premium payments between your company and the employees. Many businesses select a suboptimal ratio, which eventually drains their cash flow. Most business owners realize that higher employer contributions inspire employee loyalty. But this is not always feasible.

In fact, some firms also consider alternative options, like health stipends or monthly allowances. Some negotiate discounts with health centers and diagnostic clinics. This lets employees enjoy subsidized rates and take charge of their health. These facilities often have family packages with tailored plans for women, children, and older adults.

Consider Family Coverage as a Retention Tool

In these stressful times, a workplace that recognizes the need for health insurance for the entire family can have a competitive edge. This is why some small businesses now facilitate family coverage plans for their employees. Plans that offer health insurance for married couples cover an employee’s spouse and kids.

It is hardly a stretch to say that insurance coverage can become a solid retention tool. A 2025 SHRM Employee Benefits Survey found that 78% of employees value the available benefits when deciding whether to remain in a position. This percentage is over 80 among younger employees (25 to 44). This is noteworthy for small businesses, as high attrition can increase their operational and talent acquisition costs.

The prime advantage of family health plans is that they simplify things for the employee, drastically reducing the mental load. As LIFE143 observes, comprehensive family coverage is often (but not always) the most economical path for couples. They need only manage one deductible, network, and set of rules.

Depending on what makes financial sense for your business, you can develop such family options to improve employee satisfaction. Some employers charge spousal surcharges of up to $200 monthly if the spouse also gets coverage elsewhere. The main thing is that surcharges should not start being punitive.

Focus on Standout, But Critical, Benefits

One powerful way for small businesses to make a lasting impact on current and prospective employees is through intuitive health coverage. This concerns benefits that matter immensely in everyday life, but are not always available. Not even in bigger firms.

Consider mental health support. We live in times when awareness of mental health concerns is slowly improving. However, assistance and understanding are still very limited. Even when coverage is extensive, accountability and accessibility gaps remain.

The 2025 EBRI Employer Mental Health Survey noted that almost 97 percent of employers in the sample offered mental health benefits. This sample focused on medium and large employers. Even then, their analysis of employee utilization data was inadequate. This means that many workers were not seeking timely intervention or accessing preventative services.

In mental healthcare, affordability remains a significant roadblock. It is also one that very few firms are ready to be responsible for. This contrasts sharply with the fact that almost 80 percent of employers feel they can make a difference in pricing and quality.

The situation is similar for other highly in-demand benefits such as telemedicine and maternity care. Some employers also provide support for unfortunate events like pregnancy loss, which is often connected to depression. Another emerging area is menopause support benefits, which can help many women find the strength and understanding they need to keep advancing in their careers.

“When we leave women to figure menopause out alone, we pay a grave price in health, productivity, and our very own dignity. We have to improve access to quality care, and we need to invest in research and innovation.” – Halle Berry, Public Ambassador, Global Alliance for Women’s Health.

In this scenario, a business that is willing to go the extra mile to safeguard employees’ physical and mental health is bound to have an edge.

FAQs

1. Is it mandatory for small firms to provide health insurance to workers and their spouses?

No, these requirements vary by country and company size. In many regions, small businesses are not legally required to provide health insurance benefits. That said, providing health coverage can significantly strengthen employee satisfaction and retention. It helps businesses compete for talent.

2. What is the most affordable way for a small company to provide employee health benefits?

As a small business owner, you can control costs through group health insurance plans or health reimbursement arrangements. You can also consider telemedicine benefits or employer-funded health stipends. The most suitable pick for you will depend on workforce size, needs, and budget.

3. Should small businesses include spouse and family coverage in health plans?

Including spouse and family coverage can be a valuable retention tool, especially for married employees and those with children. Family coverage does increase costs. Still, many employers find that it improves employee loyalty and reduces turnover.

Small Firms and Employee Health Support: At a Glance

A Healthier, More Productive Workforce

As you develop health coverage plans for your team, keep the end goal in mind: building a healthier team to enhance individual and organizational productivity. When employees perceive that their employer genuinely cares for their well-being, it becomes a factor they consider when making critical career decisions. Moreover, the reassurance of having health support directly improves focus and productivity at work.

When companies view these expenses as strategic investments, it becomes a win-win situation.